Buying a TIC in San Francisco: What You Need to Know

What is a TIC in San Francisco?

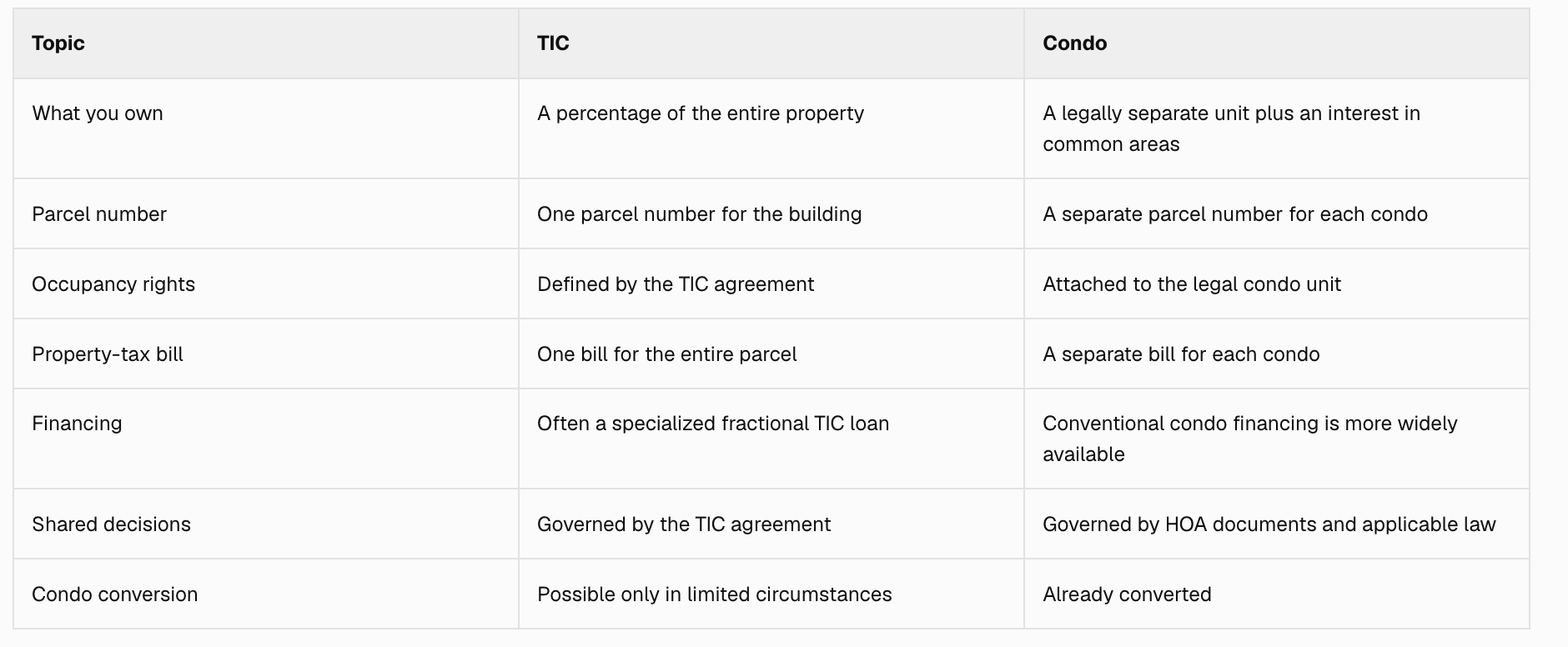

A tenancy in common is a form of shared real estate ownership. Two or more people own percentage interests in one legal parcel. A TIC building might contain separate flats, but the city still treats the property as a single parcel with one Assessor Parcel Number.

Your deed shows your ownership percentage, not legal title to a separate unit. Your exclusive right to live in a specific flat usually comes from the TIC agreement signed by the co-owners.

That is the central difference between a TIC and a condominium. A condo is a separately mapped legal parcel. A TIC is a share of one larger parcel.

According to the San Francisco Assessor-Recorder, when one TIC share changes hands, that percentage of the property is generally reassessed at current market value. The remaining shares do not automatically get reassessed just because one co-owner sells. California’s property-tax rule for tenancies in common provides the broader state framework for when a transferred TIC interest counts as a change in ownership.

TIC vs. condo: the quick comparison

Quick facts comparing TIC and Condos

How TIC financing works

Many San Francisco TIC buyers use fractional financing. With a fractional TIC loan, each owner obtains a separate loan secured by that owner’s percentage interest in the property. This is different from an older group-loan structure, where multiple owners share one mortgage.

Fractional financing can reduce the risk that one owner’s missed mortgage payment directly affects every other owner’s loan. However, TIC loans are specialized products. The pool of lenders may be smaller, underwriting can differ from conventional condo lending, and terms may be less flexible.

For example, Bank of Marin publicly offers fractional financing for owner-occupied TIC units in San Francisco. Product availability, rates, loan limits, down-payment requirements, and underwriting standards can change, so get preapproved for the specific property type before relying on a budget.

Ask prospective lenders:

Do you finance fractional TIC interests in San Francisco?

What down payment do you require?

Is the loan fixed-rate or adjustable?

Is there a prepayment penalty?

How do you review the TIC agreement and building finances?

Are taxes and insurance escrowed?

What happens if another co-owner defaults on an obligation?

Will planned construction or an unauthorized unit affect approval?

Do not assume that a preapproval for a condo will transfer to a TIC purchase.

Read the TIC agreement before you remove contingencies

The TIC agreement is the building’s operating manual. It should clearly explain the rights and responsibilities of every owner.

Have a San Francisco real estate attorney who understands TIC ownership review the agreement. If you need a starting point, the Bar Association of San Francisco’s real estate lawyer referral service specifically handles TIC and property-ownership matters. The State Bar of California also maintains a directory of certified referral services.

Important provisions include:

The unit and any storage, parking, deck, yard, or roof area assigned to you

Each owner’s percentage interest

How monthly expenses and property taxes are divided

Voting rules for repairs, improvements, budgets, and new rules

Reserve requirements and special assessments

Insurance responsibilities

Rules for leasing, pets, remodeling, and use of common areas

Procedures when an owner fails to pay

Dispute-resolution requirements

Sale, transfer, and refinancing procedures

Rights of first refusal, if any

What happens after major damage or a total loss

Pay attention to voting thresholds. Requiring unanimous approval for every meaningful decision can create gridlock. Giving one owner too much unilateral authority can create a different problem.

The agreement should also match how the building operates in practice. If the paperwork assigns parking one way but the owners follow a different arrangement, resolve the inconsistency before closing.

Understand the shared property-tax bill

San Francisco sends one property-tax bill for the entire TIC parcel, not a separate bill to each owner. Co-owners must arrange how to collect and pay their respective shares.

The Assessor-Recorder’s TIC fact sheet warns that all co-owners are responsible for ensuring the full bill is paid. A missed contribution by one owner can create penalties or other consequences for the group.

Ask to review:

The most recent property-tax bills

Proof that the bills were paid on time

The allocation method used by the owners

Any supplemental assessments

The process for collecting funds before each deadline

TIC owners can request an individual assessed-value notice from the Assessor-Recorder, but that notice does not create separate tax bills. At closing, the transfer may also require a Preliminary Change of Ownership Report, which helps the Assessor evaluate the transaction.

TIC buildings may also have Rent Board obligations. San Francisco’s Rent Board fee and Housing Inventory guidance states that TIC co-owners are jointly responsible for the property’s annual Rent Board fee, regardless of ownership share.

Review the building, not just your unit

You are buying an interest in the whole property. Your inspection and document review should extend beyond the rooms you plan to occupy.

Consider reviewing:

Roof, foundation, exterior, plumbing, electrical, heating, and seismic condition

Pest and general property inspections

The building’s Report of Residential Building Record, commonly called a 3R report

The legality of added rooms or dwelling units

Zoning, past projects, active complaints, and historic-resource information

Environmental conditions, flood zones, soil issues, and hillside review flags

Insurance policies, recent claims, deductibles, exclusions, and replacement-cost assumptions. The California Department of Insurance offers a residential insurance shopping guide.

Reserve balances and expected capital projects

Meeting minutes, budgets, invoices, and owner correspondence

Pending disputes between owners

Past-due payments or special assessments

Rental and eviction history

For an older San Francisco building, deferred maintenance can quickly outweigh an apparent discount. If the roof, foundation, sewer lateral, or exterior needs work, understand your allocated share and whether the other owners have the cash and willingness to proceed. The city’s Property Condition Assessment guidance explains where to check permit history, complaints, notices of violation, zoning, and inspection dates.

Check the tenant and eviction history

Tenant history can affect future use, resale, and possible condo conversion. It can also create legal obligations that are easy to miss during a fast transaction.

If the property has an Ellis Act history, review the recorded documents and constraints with qualified counsel. San Francisco’s Rent Board guidance explains that withdrawn units can be subject to vacancy controls and former-tenant re-rental rights for defined periods.

Ask for disclosures covering current and former tenants, owner move-in evictions, Ellis Act filings, buyout agreements, and notices recorded against the property. Do not rely only on a seller’s summary. Confirm the history through the available city and title records, including the Rent Board’s public records process and the Department of Building Inspection’s record archive.

Do not count on condo conversion

Some buyers view a TIC as a condo that has not converted yet. That assumption can lead to overpaying.

San Francisco condominium conversion is tightly regulated. The current Public Works subdivision page lists residential conversion materials for two-unit buildings and shows the Expedited Conversion Program for two-to-six-unit properties as suspended. A two-unit, separately owned, owner-occupied building may have a path to conversion after meeting applicable occupancy and other requirements, but eligibility is property-specific.

Treat conversion as a possible future benefit only after a qualified attorney and conversion specialist review the building’s unit count, ownership, occupancy, permit, tenant, and eviction history. Base your purchase decision on the TIC you are buying today.

Think ahead to resale

A TIC can be sold, but the buyer pool may be narrower than for a comparable condo. Future buyers will face the same specialized financing and document review.

Before you buy, ask:

Is your unit financed with a fractional loan or tied to a group loan?

Does the TIC agreement restrict transfers?

Must other owners approve a buyer or lender?

Is there a right of first refusal?

Are the building records organized and current?

Are reserves adequate?

Could unresolved permits or disputes complicate financing?

Clean records, clear agreements, stable building finances, and documented maintenance can make a future sale easier.

San Francisco TIC buyer checklist

Before removing contingencies, confirm that you have:

TIC-specific loan preapproval for the property

Attorney review of the TIC agreement and title documents

Inspections covering the entire building

Permit, violation, and unit-legality review

Current insurance information and coverage confirmation

Property-tax bills and payment records

Building budgets, reserves, meeting notes, and planned repairs

A clear understanding of parking, storage, decks, and other exclusive-use areas

A resale plan that does not depend on condo conversion

Is a TIC right for you?

A well-run TIC can be a practical way to buy in San Francisco. The best candidates are comfortable with shared decisions, willing to study the agreement, and prepared to evaluate the entire building rather than only one flat.

The purchase deserves a TIC-experienced team: a local agent, lender, inspector, title professional, insurance adviser, and real estate attorney. With the right diligence, you can judge whether the price advantage is worth the added complexity.

Considering a TIC in San Francisco? Talk with a local TurboHome agent before you make an offer. We can help you compare the property, financing structure, disclosures, and likely resale considerations.

This article is for general educational purposes and is not legal, tax, lending, or insurance advice. TIC rules and loan products can change. Consult qualified professionals about your specific property and circumstances.

Frequently asked questions

Is a San Francisco TIC the same as a condo?

No. A condo is a separately mapped legal parcel. A TIC buyer owns a percentage of one larger parcel and typically receives the exclusive right to occupy a specific unit through a TIC agreement.

Can I get a separate mortgage for a TIC?

Often, yes. Some lenders offer fractional TIC loans secured by one owner’s percentage interest. Availability and terms vary, so obtain TIC-specific preapproval before making financing assumptions.

Do TIC owners receive separate property-tax bills?

No. San Francisco issues one property-tax bill for the parcel. The co-owners arrange payment among themselves, and the full bill must be paid to avoid penalties.

Can every TIC convert to condos?

No. Conversion eligibility depends on the building, unit count, ownership and occupancy, permit history, tenant history, eviction history, and current city rules. Buyers should not assume conversion will be available.

What is the most important TIC document?

The TIC agreement is central because it assigns occupancy rights and governs expenses, repairs, voting, defaults, transfers, and use of the property. Have TIC-experienced counsel review it before you remove contingencies.

Sources and buyer resources

San Francisco Assessor-Recorder: Tenancy-in-common units — ownership structure, assessment, and individual assessed-value notices

San Francisco Assessor-Recorder: Thinking of Purchasing a TIC? — parcel billing, property-tax responsibility, reassessment, and TIC-versus-condo distinctions

California Board of Equalization: Property Tax Rule 462.020 — change-in-ownership rules for tenancy-in-common interests

San Francisco Assessor-Recorder: Preliminary Change of Ownership Report — ownership-transfer reporting form

San Francisco Public Works: Subdivisions and Mapping — current condominium-conversion resources and program status

San Francisco Rent Board: Evictions Pursuant to the Ellis Act — withdrawal procedures, recorded constraints, and re-rental rights

San Francisco Rent Board: Evictions — overview of local eviction rules and resources

San Francisco Rent Board: Fee and Housing Inventory — TIC co-owner responsibility for fees and reporting

San Francisco DBI: Records Management — permit records, plans, job cards, complaints, and 3R reports

San Francisco DBI: Request Public Building Records — instructions for obtaining permits, plans, certificates, and residential records

San Francisco DBI: Property Condition Assessment Guidance — permit, complaint, violation, zoning, and inspection lookups

San Francisco Planning: Property Information Map and Permits — zoning, past projects, active complaints, environmental information, and historic status

San Francisco Planning: Find My Zoning — address and block-lot zoning lookup

SF.gov: Environmental Property Information — flood, soil, groundwater, pollution, archaeology, and hillside review flags

California Department of Insurance: Shopping for Residential Insurance — policy-shopping and coverage guidance

Bar Association of San Francisco: Real Estate Lawyer Referral — TIC and property-ownership attorney referrals

State Bar of California: Certified Lawyer Referral Services — statewide certified referral directory

Bank of Marin: Tenants in Common Loans — example of currently advertised fractional TIC financing in San Francisco